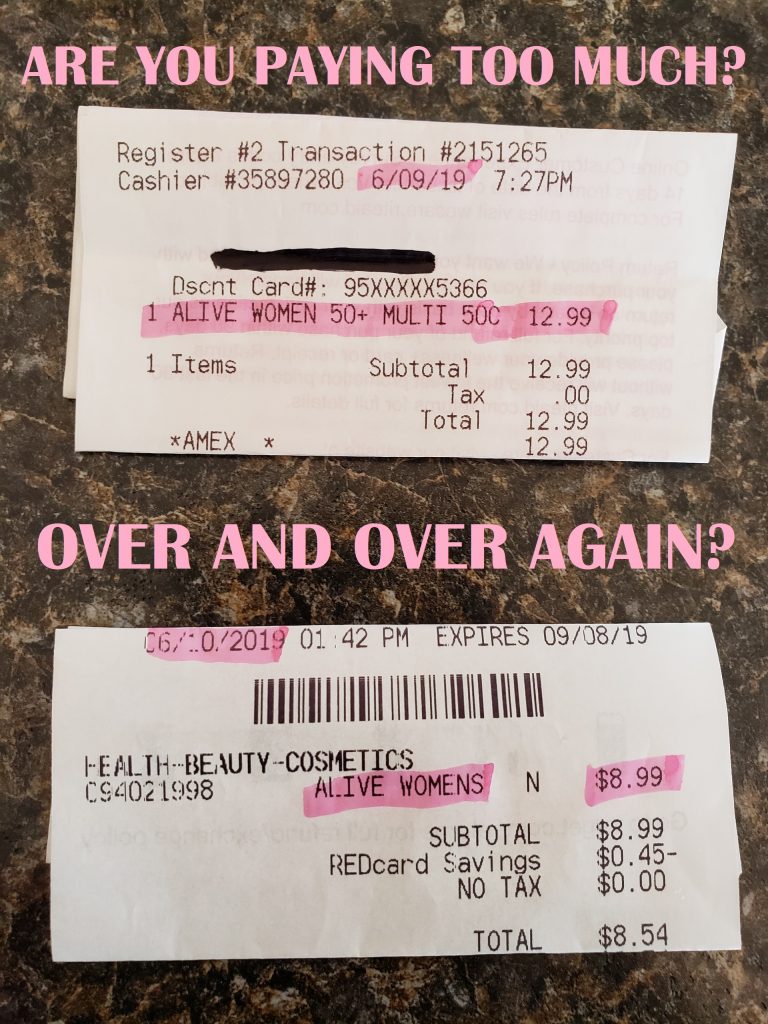

It was all my fault, and I take full responsibility. I was tired. I was lazy. I was driving by a pharmacy and remembered I had just run out of my vitamins. So I impulsively stopped to grab them. The cashier rang them up and told me the total: $12.99. I thought it seemed like more than I had been paying, but I was tired and I needed them. All the way home, my tired brain kept saying, that seems really expensive for those vitamins. As soon as I got home, I looked up the prices. WHOA, it was $4 more than where I usually buy them. Well, I need the vitamins, but 50% more just seemed more than I could bear. I tried to rationalize the purchase. I can afford it. I was tired. It is OK. But that means if I keep spending an extra $4 for vitamins over the course of a year, I would spend an extra $48 on vitamins when I really could’ve gotten them cheaper. That’s what a dinner out might cost. What if I spent an extra $4 on ten other products? $48 x 10 = $480. Now, that could be a plane ticket or two. I’d rather have a trip to Maui than paying a convenience fee of $4. Back to the store I went to return the high priced vitamins. Then I went where I regularly buy them for a much lower price. It certainly cost more to right this wrong but the moral of the story is: I have my $4 back, my dinner out, my plane tickets to Maui, and I learned my lesson (maybe you did too)!

It was all my fault, and I take full responsibility. I was tired. I was lazy. I was driving by a pharmacy and remembered I had just run out of my vitamins. So I impulsively stopped to grab them. The cashier rang them up and told me the total: $12.99. I thought it seemed like more than I had been paying, but I was tired and I needed them. All the way home, my tired brain kept saying, that seems really expensive for those vitamins. As soon as I got home, I looked up the prices. WHOA, it was $4 more than where I usually buy them. Well, I need the vitamins, but 50% more just seemed more than I could bear. I tried to rationalize the purchase. I can afford it. I was tired. It is OK. But that means if I keep spending an extra $4 for vitamins over the course of a year, I would spend an extra $48 on vitamins when I really could’ve gotten them cheaper. That’s what a dinner out might cost. What if I spent an extra $4 on ten other products? $48 x 10 = $480. Now, that could be a plane ticket or two. I’d rather have a trip to Maui than paying a convenience fee of $4. Back to the store I went to return the high priced vitamins. Then I went where I regularly buy them for a much lower price. It certainly cost more to right this wrong but the moral of the story is: I have my $4 back, my dinner out, my plane tickets to Maui, and I learned my lesson (maybe you did too)!

trade

Tax Refund? What are you going to do with it?

We have some suggestions if you want to create a feeling of financial freedom.

We have some suggestions if you want to create a feeling of financial freedom.

(1) Pay debts – Use the refund to pay debts that are from consumption or non-appreciating assets like credit card debt, student loans, car loans, medical debts, etc.

(2) Fund expected and unexpected expense saving accounts – Creating these reserves to draw from when necessary can avoid you from creating debt when life events occur.

(3) Invest it – There are so many opportunities to grow your money. We generally suggest the stock market, real estate, or businesses.

(4) Create a fun fund – If you have all your debts paid off, fully funded expected and unexpected saving accounts, and you are investing consistently a percentage of your income regularly, it is time to have some fun! You can save it up for something big or use it for some special occasions.

If your refund is large, you may want to look at adjusting your withholding or your estimated tax payments.

Above all else, always consider using your refund to improve your financial situation.